ABC of Section 7C and the Tax Implications

Delecia Venter | Tax Director, PKF Port Elizabeth

THE ABC’S OF DEEMED DONATIONS UNDER SECTION 7C AND THE TAX IMPLICATIONS

A. ABOUT SECTION 7C

Section 7C is an anti-avoidance provision, which specifically targets low or interest-free loans made to a trust at the behest of an individual or a company that is connected to that individual. This provision was initially introduced on 01 March 2017. Its primary objective is to prevent taxpayers from shifting their wealth assets by way of sale to family trusts on loan account.

This shifting of wealth effectively “pegged” the value of the asset in the hands of the taxpayer by replacing it with the loan account (either interest-free or at a low rate of interest). The value of the asset continued to increase in value in the trust, thereby avoiding various taxes that the individual taxpayer would otherwise be subject to, such as Donations Tax, additional Capital Gains Tax, and Estate Duty.

Section 7C has been amended over the years to close possible tax loopholes. Here is a breakdown of some of the key amendments:

• The provision was extended to include low or interest-free loans made to companies in which a trust holds at least 20% of the equity shares or voting rights.

• The provision was extended to the subscription of preference shares in a company by individuals, where 20% or more of the equity shares are held, or the voting rights in the company can be exercised by a trust that is a connected person in relation to that individual or company.

B. BASICS OF SECTION 7C

Section 7C requires that an interest charge be imputed on a low or interest-free loan made to a trust (both local and foreign) or to a company owned by a trust (both local and foreign). Where the loan is made to a foreign trust or company, the general transfer pricing rules, which require that the loan must be at arm’s length, must be applied; thereafter, Section 7C must be considered. The imputed interest charge is consequently treated as a deemed donation for tax purposes.

The imputed interest charge is the difference between the actual interest charged and the SARS official rate of interest. Essentially, the foregone interest is treated as a deemed donation and subject to Donations Tax.

The deemed donation is calculated annually in relation to each year of assessment that the loan balance remains outstanding by the trust or company. The deemed donation is to be treated as a donation made by an individual to a trust or company on the last day of the year of assessment of that trust or company, respectively. Trusts' years of assessment generally end on the last day of February of each year.

Therefore, taxpayers in preparation for their 2024/2025 tax obligations are reminded that Donations Tax resulting from their low or interest-free loans to trusts or companies with a February year-end will be due and payable to SARS by 31 March 2025. To avoid any late payment penalties and interest, it is important for taxpayers to review any outstanding loans with trusts and companies to determine whether they have a potential tax liability. Taxpayers are urged to consult with a registered tax professional for any assistance. We, at PKF, can help navigate this process and assist with full compliance.

C. COMPUTATION OF SECTION 7C DEEMED DONATION

Below are examples to help illustrate the calculation of the deemed donation:

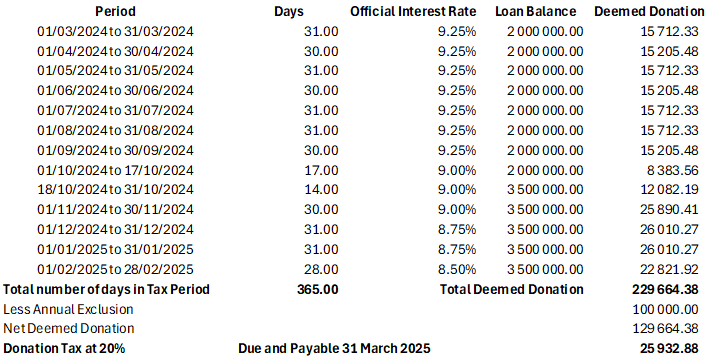

EXAMPLE 1: INTEREST-FREE LOAN

Mr. Soap lends R2 million interest-free to his family trust on 01 March 2024 and again R1.5 million on 18 October 2024. Mr. Soap chose to apply his annual donation tax exemption of R100,000. The deemed donation (foregone interest) and donation tax liability under Section 7C are calculated as follows as at the last day of February 2025:

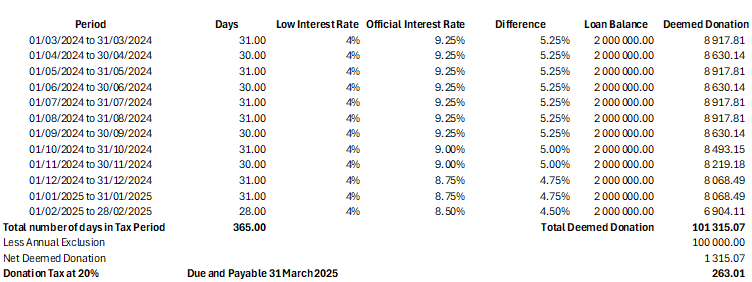

EXAMPLE 2: BELOW-MARKET INTEREST RATE

Mrs. Jones lends R2 million to her family trust on 01 March 2024 at an interest rate of 4%. She chose to apply her annual donation tax exemption of R100,000. The deemed donation (foregone interest) and donation tax liability are calculated as follows as at the last day of February 2025:

CONCLUSION

The implications of Section 7C can be rather complex due to various reasons such as:

• The multiple changes to the SARS official rate over the year of assessment, as seen in the examples above.

• Movements in the loan account during the year of assessment.

• Whether any of the relevant exemptions apply to the whole or part of the loan.

• Example: A loan balance may comprise various amounts, some of which may have been used to fund a primary residence, which would qualify for an exemption from Section 7C. The balance of the loan, however, may still be subject to the deemed donations rules of Section 7C.

• Where a loan has been outstanding for a long time, it may be difficult to analyze and determine what that loan balance comprises to see if any exemptions apply.

As a result of the many complex issues that may arise, some of which are noted above, we recommend that you seek professional advice before making any submissions of deemed donations. This ensures proper compliance and limits exposure to potential penalties and interest for adopting incorrect tax treatment.