Shining the Spotlight on the IRBA’s Reportable Irregularities Process

Serika Rambaran | Associate Director, PKF Durban

The Independent Regulatory Board for Auditors (IRBA) issued its inaugural report (the report) on the Reportable Irregularities (RI) process on 15 November 2024. The RI process, as outlined in Section 45 of the Auditing Profession Act (APA), places a responsibility on the auditor to assess whether an unlawful act or omission meets the definition of a RI, and if so, to report the RI in good faith, based on the information that has come to the auditor’s attention. For an RI to exist, there must be an unlawful act or omission on the part of a person responsible for management of an entity. It is therefore critical that management understand and recognise their responsibilities to manage the related entity in compliance with applicable laws and regulations.

In the CEO’s Foreword, Imre Nagy (IRBA CEO) explained that the objective of issuing the report was to enhance transparency, increase regulatory collaboration, and bolster stakeholder confidence in the audit profession; adding that audit committees, boards, investors, and the public will gain valuable insights into risk areas that necessitate increased scrutiny within South Africa’s corporate landscape. Through the report, the IRBA provides feedback on the nature of RIs reported over a specific period and the measures taken to address them. The report covers a five – year overview of RIs and a detailed analysis focused on the 2022/2023 fiscal year that ended on 31 March 2023.

A Brief Summary of the Statistics and Trends

Overall analysis of reports received

The report highlights that the majority of all RIs relate to contraventions of the Companies Act 71 of 2008 and the Income Tax Act 58 of 1963. Other notable areas of contraventions related to the Unemployment Insurance Act 63 of 2001, the Value-Added Tax (VAT) Act 89 of 1991 and irregularities in the basic education sector.

Section 45 of the APA places a responsibility on an individual registered auditor of an entity who is satisfied or has reason to believe that an RI has taken place or is taking place in respect of that entity to, without delay, send a written report to the IRBA. Accordingly, the IRBA received a total of 622 RI reports (“first reports”) from auditors during the 2022/2023 reporting period.

The APA further requires that the auditor follow a process which includes (inter alia) submitting a second report to the IRBA within 30 days from the date of the first report. The second report must include, among other things, a statement that the registered auditor is of the opinion that no RI has taken place or is taking place; or the suspected RI is no longer taking place and that adequate steps have been taken for the prevention or recovery of any loss as a result thereof, if relevant; or the RI is continuing. The related second reports received by the IRBA indicated that 411 RIs were of a continuing nature, 202 RIs were not continuing and 9 irregularities that were initially reported did not occur.

The content of the first and second reports received were analysed by the IRBA and detailed feedback was provided in the report.

This article summarises some of these key insights below:

• RI Reports per Province

Whilst RI reports were received from auditors practising in all nine of South Africa’s provinces, the analysis performed identified that 90% of all reports received were sent by auditors practising in three major provinces being, Gauteng (63,8%), Western Cape (13,5%) and KwaZulu-Natal (13%). The report explained that the results from the analyses was expected due to the magnitude of economic activities in these provinces.

• Types of Legal Entities reported

Irregularities were reported in relation to audits performed by auditors on various types of legal entities. Based on the analyses performed by the IRBA, it appears that the main types of audited entities to which the 1244 RI reports relate, were private companies (31.8%), body corporates (29.3%) and schools (10,6%). Non – profit organisations (5,8%) and attorney firms trust accounts (3,4%) round up the top five types of entities in respect of which RIs were reported.

• RI Reports by Industry

The analyses performed by the IRBA, revealed that most of the RI reports received related to the property management industry (39.7%). The property management industry relates to body corporates, homeowners’ associations and estate agency firms. Other contributing industries of note are the basic education sector (10.8%), social welfare entities and NPOs (6.6%) and those in the manufacturing industry (4.7%).

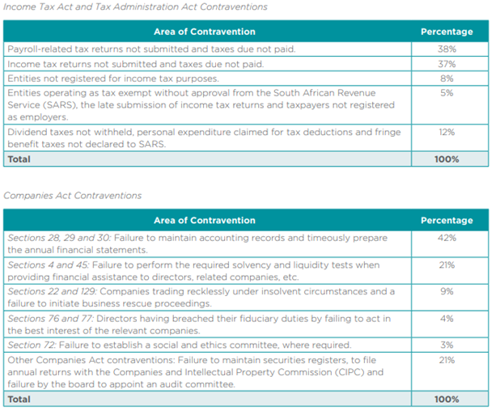

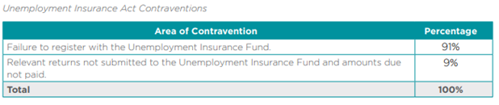

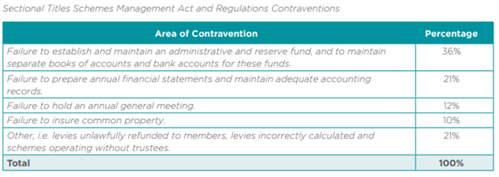

Analysis of second RI Reports

The analysis performed by the IRBA on the 411 continuing RIs communicated through the second RI reports, provides an indication of the nature of contraventions (irregularities) that were reported as continuing.

It is critical that management take note of these areas of contraventions (including the more detailed information provided in the table below), assess whether the same deficiencies may exist within their organisation, and apply remedial measures to address these deficiencies.

Based on the analysis performed, it appears that contraventions related to the following laws and/regulations appear to be most prevalent (making up 80% of all continuing RIs):

o the Tax Administration Act,

o the Income Tax Act,

o The Companies Act and Regulations,

o the Unemployment Insurance Act,

o the Sectional Titles Schemes Management Act and Regulations and

o the VAT Act.

The analysis included in the table below (table extracted from the IRBA’s report) provides further information related to the specific sections within the laws and regulations mentioned above that were contravened.

IRBA Onward Transmission of RI Reports to Other Regulators

As per the requirements of Section 45(4) of the APA, continuing second reports received by the IRBA are onward transmitted to the appropriate regulators for further consideration and/or investigation. It was noted that the main regulators to whom most of the reported continuing irregularities were sent for appropriate action were SARS (35%), CIPC (18%) and the Department of Employment and Labour (including UIF) (26%).

Conclusion

It was noted that the nature of the reportable irregularities reported related to, what one may assess as “basic” responsibilities of management. Management is cautioned that non - compliance with such responsibilities may be viewed as negligent on the part of management in upholding their fiduciary duties and may result in severe repercussions.

The IRBA’s report encourages management and boards “to respond proactively to the RI process and effect the necessary remedies to ensure that RIs are resolved promptly.

Auditors are obliged to ensure that all stakeholders (shareholders, creditors, the fiscus, the public at large), are protected, and that management are held accountable if found to be failing in their duties to ensure compliance with laws and regulations.

IRBA’s concluding remarks to this report highlight the importance of Section 45 of the APA and the role it plays as being “critical in enhancing investor confidence in the South African economy.”