VAT Increase to 15.5% on 1 May 2025 - Practical Implications

Michelle Hawkins | Senior Tax Specialist, PKF Octagon

Introduction

The increase in VAT by 0.5% has significant implications for businesses and individuals, particularly for ongoing transactions that have not yet been completed. Before diving into the “nitty-gritty” of which rate is applicable across the various types of transactions, consideration must first be given as to the immediate actions that need to be taken by businesses.

Pre-printed Notices or Price Lists

For retail and similar environments, businesses may display a notice stating that prices exclude the VAT increase and will be adjusted at checkout. This notice can remain until August 31, 2025.

However, it must be displayed clearly and all labelling and prices on shelves should either reflect excluding VAT or be displayed continuously throughout the shop to avoid any issues. For pre-printed invoices, businesses may continue using them for six months after 1 May 2025, if they manually adjust the VAT rate.

Points-of-Sale Systems and Financial Systems

Businesses must ensure that their point-of-sale systems are updated such that the tax invoices issued on or after 1 May 2025 reflect the new rate of 15.5%.

Pre-packaged financial/accounting systems which are commonly used by businesses will be updated to incorporate the new VAT rate as from 1 May 2025. Business with in-house developed software packages must be updated/re-programmed to cater for the change in rate.

Time of Supply Rules - General

Understanding the “time of supply” is crucial, as it determines when VAT liability is triggered. The general time of supply is the earlier of the invoice or the receipt of the payment.

If an invoice is raised or payment is received before 1 May 2025, the applicable VAT rate remains 15%. However, if the invoice and payment occur on or after 1 May 2025, the new VAT rate of 15.5% will apply.

Supply of Goods and Services

The old VAT rate (15%) applies if:

• Goods are supplied before the VAT rate change.

• Goods are provided under a rental agreement.

• Goods are paid for in instalments.

• Goods are supplied for construction activities.

• Services are fully performed before 1 May 2025.

For goods and services spanning the rate change (e.g., starting before but ending after 1 May 2025), a fair and reasonable apportionment must be made. However, VAT must still be accounted for in the tax period in which the supply occurs.

• Examples of affected transactions:

• Rental agreements

• Progressive payments or periodic supplies

• Construction activities

• Services spanning the VAT rate change

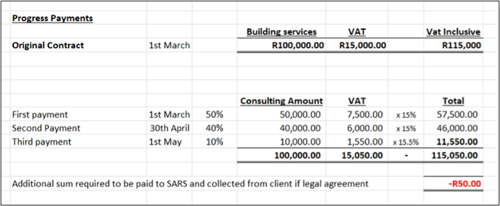

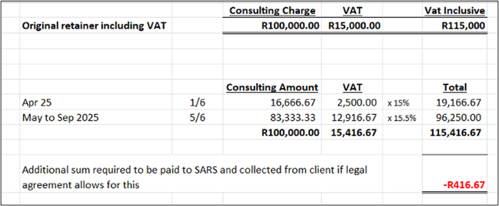

• Example: A consultant receives a retainer payment of R115,000 (including VAT) in April 2025 for services over the next six months. The VAT must be apportioned accordingly.

Time of Supply - Transitional Rules

Despite the general time of supply rules note above, the VAT Act contains certain transitional rules which apply when there is a change in the VAT rate which are outlined below.

1. Ongoing Contracts

Contracts such as property rentals, construction, cleaning, insurance, and subscription services often require advance payment at the beginning of the month. The increased VAT rate applies to any payment due or received on or after 1 May 2025.

For these contracts, the time of supply is determined by the contract itself—not by the invoice date. Therefore, invoices issued early for the period from 1 May 2025, should reflect the new VAT rate.

2. Instalment Sale Agreements and Finance Leases

These are treated differently from ongoing contracts. If goods are delivered before 1 May 2025, the old VAT rate of 15% applies. However, monthly VAT on service fees under such agreements will increase accordingly to 15.5% from 1 May 2025.

3. Commercial and residential property transactions

For property sales, the VAT rate is determined by the date of registration in the Deeds Office or the date of payment, whichever is earlier. A deposit held in trust is not considered a payment of the purchase price until it becomes non-refundable. However, the higher VAT rate will apply when time of supply is triggered

For residential property, if a written, binding legal agreement is concluded before 1 May 2025, the lower VAT rate applies—even if suspensive conditions exist. However, it is imperative that the contract must state the VAT-inclusive price.

4. Importation of Goods and Services

The VAT rate on imported goods is determined by the customs clearance date. If customs clear the goods after 1 May 2025, the new rate applies—even if they arrived earlier.

For imported services, the VAT rate is determined by the earlier of:

• The supplier issuing an invoice.

• The recipient making a payment.

5. Other Specific Types of Transactions Affected

There are other specific types of transactions which are also subject to the time of supply rules under the transitional provisions but have not been expanded on in this article. These are noted as follows:

• Supply of Goods and Services Between Connected Parties

• Estate Agent Commission

• Deposits made in respect of Guest House Accommodation

It is therefore advisable that vendors entering into any of these types of transactions should obtain professional advice to ensure compliance.

Anti-avoidance Rules

To prevent early invoicing or payments from avoiding the new VAT rate, the following transactions will be taxed at 15.5%:

• Goods supplied more than 21 days after 1 May 2025.

• Services performed more than 21 days after 1 May 2025.

These supplies are deemed to occur at the new rate and must be included in that tax return period. However, this does not apply to residential property transactions or to normal business practice which have long lead times.

Other Key Considerations

• No additional input tax can be claimed on trading stock held at the time of the VAT increase.

• Ensure suppliers correctly apply the VAT rate on invoices. Request a credit note and new invoice where the incorrect rate is applied.

• Debit or credit notes relating to transactions before 1 May 2025, must use the old VAT rate (15%).

• Tax Computation of input and output tax on VAT201 returns must contain the correct VAT rates

Conclusion

Vendors are encouraged to be proactive in implementing the VAT increase by taking steps prior to 1 May 2025 to ensure that their businesses are prepared and will be compliant levying VAT at the correct rate on any supply of goods or services.

Prices charged by vendors are deemed to include VAT hence, any under-declaration of VAT would result in reduced profit margins along with penalties and interest being imposed by SARS which may have a significant impact on businesses.

Should you require assistance in ensuring that your business remains compliant please do not hesitate to contact your nearest PKF office for assistance.