SARS Tightens the Net: Trusts May Now Face Administrative Penalties

By Michelle Hawkins, Senior Tax Specialist, PKF Octagon

On 27 March 2026, the South African Revenue Service (“SARS”) published and promulgated the notice for the imposition of fixed amount penalties for Trusts, where a Trust fails to file its tax return.

These penalties will be imposed on all incidences of non-compliance where a Trust fails to submit an Income Tax return as and when required by SARS.

SARS will now issue final demands referring to this Gazette and provide the Trust 21 business days to file the outstanding Tax Returns. The provision is applicable to the 2024 and 2025 trust tax returns onwards. We note that SARS had already started to issue final demands when the notice was still in its draft form and those trusts should contact their nearest PKF office to take further advice.

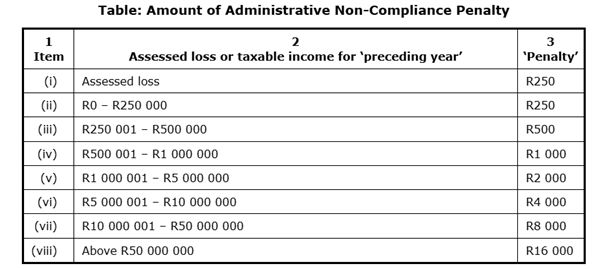

The Tax Administration Act determines the penalties to be imposed, which is based on the assessed loss or taxable income for each preceding year.

The penalty amount will be automatically imposed up to a period of 36 months, until the person remedies the non-compliance. Where SARS is not in possession of the current address of the person and is unable to deliver the ‘penalty assessment’, the 36-month period can be extended to 47 months.

Please take note that it can become a substantial tax debt if not complied with. A request for remission of penalties can only be submitted to SARS once the non-compliance has been remedied. In practice, SARS often uses third-party appointments (e.g. relevant taxpayer’s bank) to collect administrative penalties on their behalf.

Reminder for other non-compliant taxpayers

The Administrative Penalties table above also apply where a taxpayer is:

- A natural person who has one or more year’s tax returns outstanding

- A company which has returns outstanding from the 2009 tax year and failed to submit the returns within 21 days of a specific final demand.

Should you find that you require assistance to regularise non-compliance for any taxpayer type (trusts, natural person or company) please do not hesitate to contact your nearest PKF office.